What is CIBIL score

CIBIL Score is a three-digit numeric summary of your credit history. The score is derived using the credit history found in the CIBIL Report (also known as CIR i.e Credit Information Report).

A CIR is an individual’s credit payment history across loan types and credit institutions over a period of time. A CIR does not contain details of your savings, investments or fixed deposits.

CIBIL Score range

| Score Band | Category |

|---|---|

| < 300 | Poor Credit Score |

| 300-550 | Very Low Credit Score |

| 551-620 | Low Credit Score |

| 621-700 | Fair Credit Score |

| 701-749 | Good Credit Score |

| 750-900 | Excellent Credit Score |

Why you should keep a healthy CIBIL score

Everyone will need a loan from a financial institution at some point in their life for high value purchases / spends which may include the following –

- Home Loan

- Education Loan

A good CIBIL score will help you get your loan approvals very quickly without any hassles.

Disadvantages of a poor CIBIL score

If you have a CIBIL score which is less than 700 , you may find delays in your loan approvals and may end up with additional paper work and end up paying more. Some additional costs that you may incur –

- For additional paper work, you may have to approach a CA who may charge you 2-4% of the loan amount.

- Banks may charge additional processing fees of up to 0.5%

- Banks may charge additional interest of 0.5 – 1 %

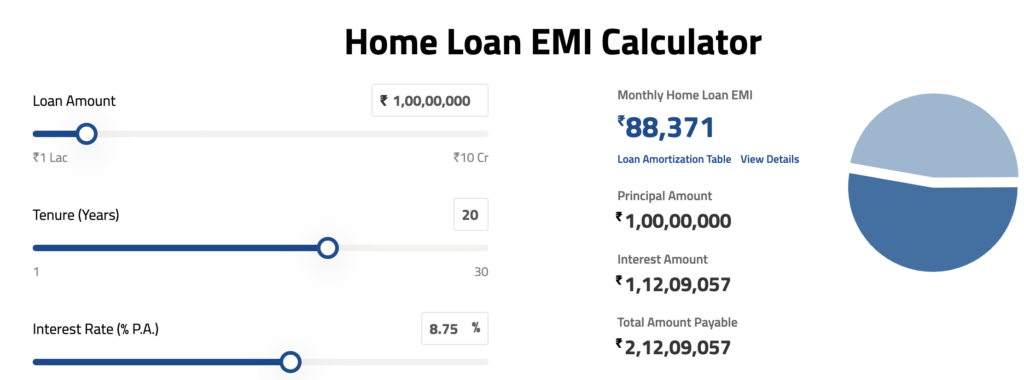

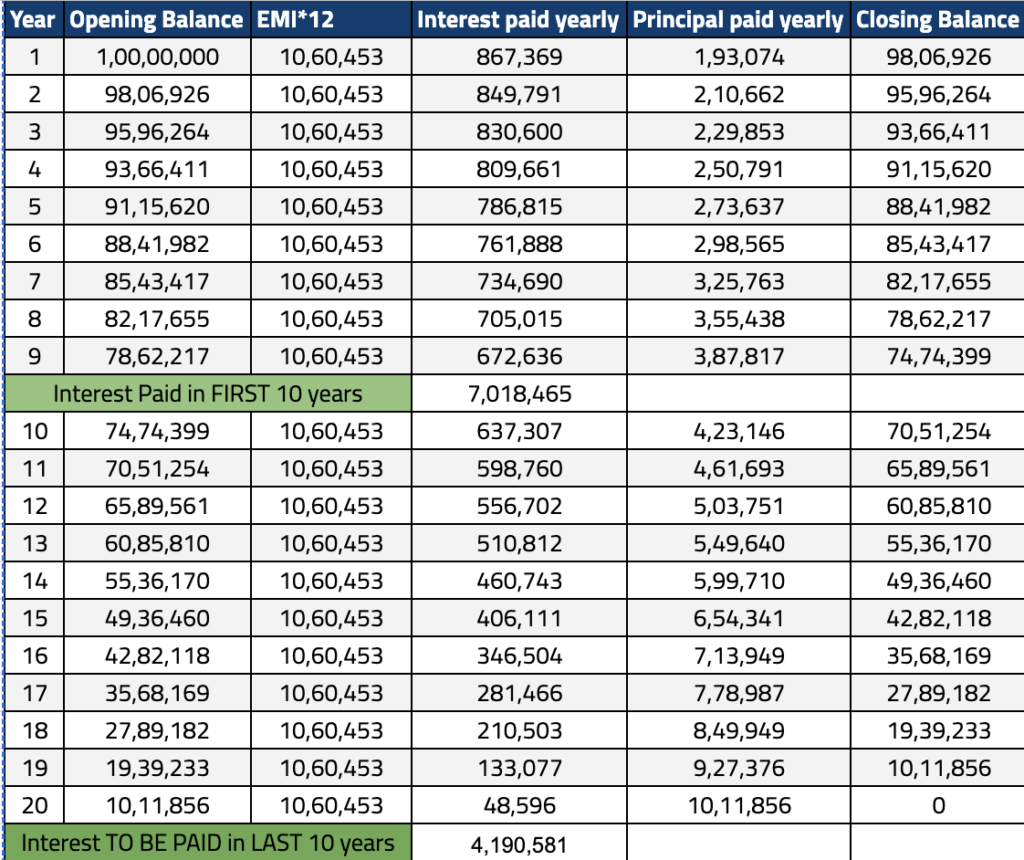

Let’s see if you have to pay these additional cost at the lower end, how much you may need to shell out from your pocket.

| Additional cost category | Appx cost for a 20 year loan of 50 lacs |

|---|---|

| Additional paper work by CA @ 2% | 1,00,000 |

| Additional processing fees by banks @ 0.5% | 50,000 |

| Additional interest by banks @ 0.5% for a 20 year loan at 8.75% | ~ 1,500 per month |

| Overall Additional Costs | 8~10 % more for your entire loan term |

Why banks will charge more

Banks lend based on risk profile of a customer. If the risk is more, banks will charge more.

It’s that simple.

For a customer with poor risk profile, probability of default is more.

Who will be happy if you have a bad CIBIL score

- CA’s – They get additional money for paper work

- Banks – They charge you additional processing fee and additional interest rate